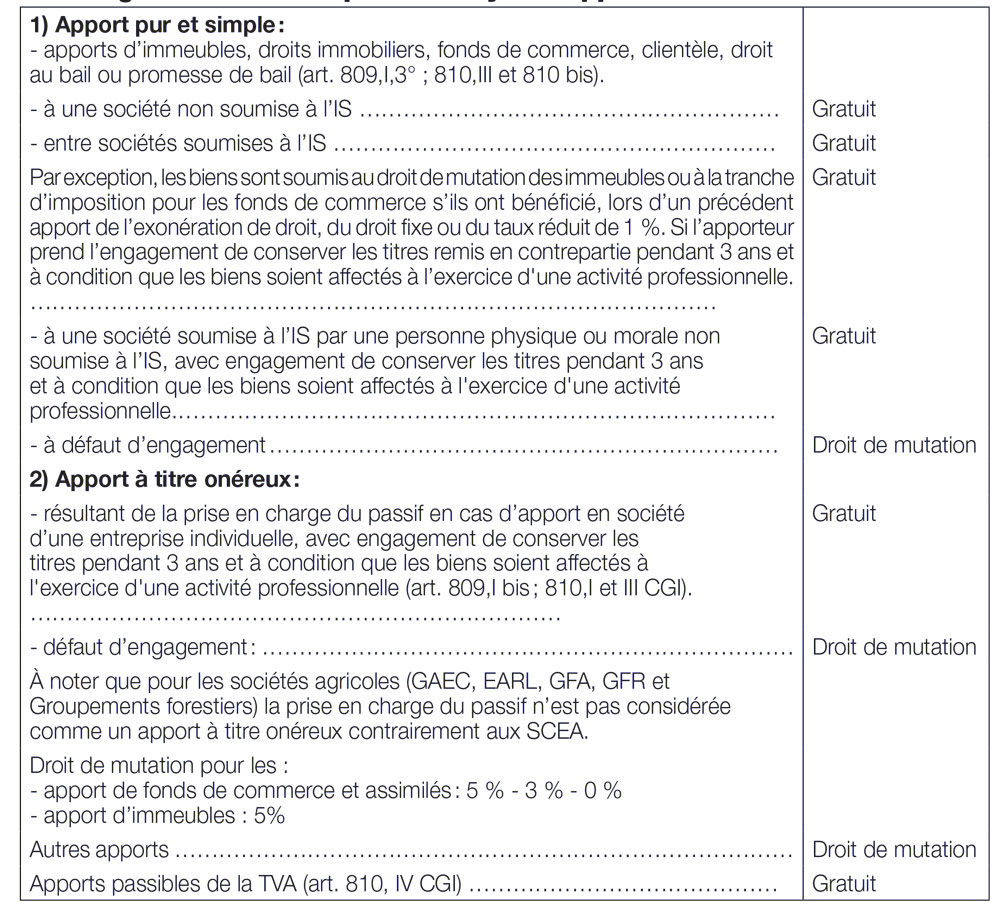

APPORT A SOCIÉTÉ. – APPORT PUR ET SIMPLE RÉALISÉ AU COURS DU FONCTIONNEMENT DE LA SOCIÉTÉ. – 94 – Augmentation de capital au moyen d’apports nouveaux.

APPORT A SOCIÉTÉ.

APPORT PUR ET SIMPLE RÉALISÉ AU COURS DU FONCTIONNEMENT DE LA SOCIÉTÉ.

94 – Augmentation de capital au moyen d’apports nouveaux.

Pour l’apport pur et simple ou à titre onéreux fait à une personne morale passible de l’impôt sur les sociétés au cours du fonctionnement de celle-ci ou à titre onéreux (voir l’article 98).